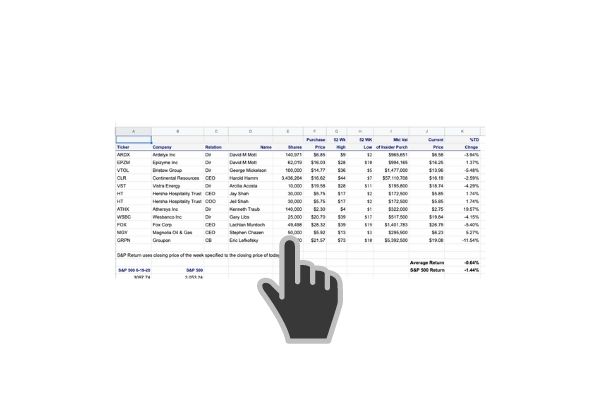

There may not have been a rush of insider buying last week but there are some definite potential home runs to ponder. None more quixotical than NGR Partners. Crimble, the CEO, has bought 1,140,000 million shares spending $7,134,034 during the last five years at every lower prices. His latest purchase was just was up 18% last week.

Then there are the CEO and CFO duo from Cano Health who purchased over $16 million dollars worth of CANO yielding gains as high as 35% in a week! I’m going to spend serious time this week on CANO as these guys are a force of nature.

If you do one thing with this email and post, look at CVR Partners. This stock went from sub $1.00 to over $58 in 18 months. The CEO buying should have tipped us off. Is NGL a repeat? I think it’s worth a shot. No one loved UAN CVR Partners before it launched. Goldman downgraded it from $5 to $3 in January 2020. It’s $58 today. Where is the Goldman analyst today?

Last but not least, remember to fall in love with people, not stocks.

Name: Krimbill H Michael

Position: CEO

Shares Bought: 200,000, Average Price Paid: $1.50, Cost: $299,950

Company: NGL Energy Partners LP. (NGL)

NGL Energy Partners LP engages in the crude oil and liquids logistics and water solution businesses. The company’s Crude Oil Logistics segment purchases crude oil from producers and marketers and transports it to refineries for resale at pipeline injection stations, storage terminals, barge loading facilities, rail facilities, refineries, and other trade hubs; and provides storage, terminaling, and pipeline transportation services. Its Water Solutions segment transports, treats, recycles and disposes of, produced, and flowed back water generated from oil and natural gas production; disposes solids, such as tank bottoms and drilling fluid and muds, as well as performs truck and frac tank washouts; and sells produced water for reuse and brackish non-potable water. The company’s Liquids Logistics segment supplies natural gas liquids, refined petroleum products, and biodiesel to commercial, retail, and industrial customers in the United States and Canada through its 28 terminals, third-party storage and terminal facilities, and standard carrier pipelines, as well as through a fleet of leased railcars. This segment is also involved in the marine export of butane through its facility in Chesapeake, Virginia, and offers termaniling and storage services. NGL Energy Holdings LLC serves as the general partner of the company. The company was founded in 1940 and is headquartered in Tulsa, Oklahoma.

Mr. Krimbill is Chief Executive Officer and also serves as a member of the Board of Directors. He has over 20 years of experience in executive roles in the propane industry. He was the past President and Chief Financial Officer of Energy Transfer Partners LP from 2004 through 2007. He was a former Director of Energy Transfer Equity, the General Partner of Energy Transfer Partners. At Heritage Propane Partners, the predecessor of Energy Transfer Partners, Mr. Krimbill, filled various roles from 1990 through 2004, including Chief Financial Officer and Chief Executive Officer. Mr. Krimbill served as a member of Williams’ Partners LP board from 2007 – 2012, where he was a member of the Audit Committee and the Chairman of the Conflicts Committee. He also served on the board of Pacific Commerce Bank from 2011-2015.

Opinion: Morgan Stanley just did an interesting podcast on Norway and how EV usage has soared there, more than anywhere else in Europe and yet hydrocarbon consumption still is on the rise there. It might lend some logic to the otherwise inscrutable, none more quixotically than NGR Partner’s CEO many purchase of NGL Partner. Crimble, the CEO, has bought 1,140,000 million shares spending $7,134,034 during the last five years at ever-lower prices.

His latest purchase was 200,000 shares at $1.50 Is it a case of don’t buy a falling knife or is it the bottom before a 20x run like CVR Partners in just 18 months. I think it’s worth a gamble. The similarities to UAN CVR Partners are startling. These MLP’s pay out the majority of their earnings each quarter. NGL started reducing its distribution in April of 2020 and stopped it altogether in November 2020 at $.10 per share.

This is a leveraged bet on the sustainability of the hydrocarbon economy and we may have to only look at Norway for an answer to this. When I read the earnings transcript on Seeking Alpha. not one analyst asked Krimbill to explain why he continues to buy this stock on the way down.

.

Name: Pytosh Mark A

Position: CEO

Shares Bought: 5,000, Average Price Paid: $58.45, Cost: $292,245

Company: CVR Partners LP. (UAN)

CVR Partners LP (NYSE: UAN) is a publicly traded company based in Sugar Land, Texas that manufactures and provides nitrogen fertilizer products. It is a subsidiary of Coffeyville Resources, which CVR Energy Inc owns. The company was formed by CVR Energy to operate its nitrogen fertilizer business. CVR Energy, Inc. was listed as a 2012 Fortune 500 company with NO.5 ranking in Houston Chronicle. CVR Partners is a growth-oriented company focused on producing nitrogen fertilizer to help serve the needs of a growing population. Their company uses state-of-the-art technologies to produce urea ammonium nitrate (UAN) and ammonia fertilizer products while remaining committed to unitholder value and safe and environmentally conscientious operations. The CVR Partners nitrogen fertilizer plant is the only such operation in North America that uses a petroleum coke gasification process to make hydrogen, a key ingredient in its manufacturing process. It produces about five percent of total UAN demand in the U.S. As a growth-oriented limited partnership formed by CVR Energy, Inc. to own, operate, and grow their nitrogen fertilizer business, CVR Partners fertilizer manufacturing facility is located in Coffeyville, Kansas, and East Dubuque, Illinois. Coffeyville Resources Nitrogen Fertilizers is a wholly-owned subsidiary of CVR Partners and directly owns and operates the CVR Partners nitrogen fertilizer plant.

Mr. Pytosh serves as Chief Executive Officer, President, and a Director of the general partner of CVR Partners, LP, and Executive Vice President, Corporate Services for CVR Energy, and Executive Vice President, Corporate Services for the general partner of CVR Refining, LP. He also serves as Chairman of the Board of Directors’ environmental, health and safety committee for CVR Partners. Before joining CVR Partners, Mr. Pytosh served as Executive Vice President and Chief Financial Officer for Alberta, Canada-based Tervita Corporation, an environmental and energy services company.

Opinion: Wow I really wish I had bought CVR Partners when Goldman downgraded it to $3 in January 2020. How many stocks can you name that have gone up nearly 20x in a year and a half? Here’s a link to the 3rd Quarter 2020 earnings call transcript at Motley Fool This is where the turn was but how would you know? Pytash was there buying 100,000 shares at $.64 in November 2020. and he’s still buying. This makes me want to look very carefully at NGL partners where Crimbal is buying this week.

Name: Mccallister Terry D

Position: Director

Shares Bought: 10,000, Average Price Paid: $24.61, Cost: $246,100

Company: Primoris Services Corp. (PRIM)

Primoris Services Corporation is a publicly-traded specialty construction and infrastructure company, with a particular focus on pipelines for natural gas, wastewater, and water. As of 2014, it was a Fortune 1000 company. Primoris Services Corp. is a holding company, which engages in the provision of construction, fabrication, maintenance, replacement, and engineering services. It operates through the following segments: Power, Pipeline, Utilities, Transmission, and Civil. The Power segment comprises full engineering, procurement, and construction project delivery; turnkey construction; retrofits; upgrades; repairs; outages; and maintenance petroleum, petrochemical, water, and other industries. The Pipeline segment includes pipeline construction and maintenance, facility work, compressor stations, pump stations, metering facilities, and other pipeline-related services for petroleum and petrochemical industries. The Utility segment involves utility line installation and maintenance, gas and electric distribution, streetlight construction, substation work, and fiber optic cable installation. The Transmission segment specializes in electric and gas transmission and distribution, including comprehensive engineering, procurement, maintenance and construction, repair, and restoration of utility infrastructure. The Civil segment consists of highway and bridge construction, airport runway and taxiway construction, demolition, heavy earthwork, soil stabilization, mass excavation, and drainage projects. The company was founded by Brian Patt in 2004 and is headquartered in Dallas, TX.

Terry D. Mccallister was appointed a Director on July 1, 2020. Mr. McCallister has a forty-year history in nearly all aspects of the energy sector, including utilities, pipelines, clean energy, and exploration and production endeavors. He was Chairman and Chief Executive Officer of WGL Holdings, Inc. and Washington Gas from 2009 until his retirement in 2018. Prior thereto, Mr. McCallister served as President and Chief Operating Officer of WGL and Washington Gas, joining Washington Gas in 2000 as Vice President of Operations. He has also held various leadership positions with Southern Natural Gas and Atlantic Richfield Company.

Opinion: The infrastructure bill is going to provide smooth sailing for PRIM. All aboard!

Name: Aguilar Richard

Position: Chief Clinical Officer

Shares Bought: 123,406, Average Price Paid: $11.97, Cost: $1,476,554

Name: Hernandez Marlow

Position: CEO

Shares Bought: 1,319,326, Average Price Paid: $10.88, Cost: $14,350,359

Company: Cano Health Inc. (CANO)

Cano Health operates primary care centers and supports affiliated medical practices in Florida, Texas, Nevada, and Puerto Rico that specialize in value-based care for seniors. As part of its care coordination strategy, Cano Health provides high-touch population health management programs such as wellness activities, pharmacy services, home visits, telehealth, the transition of care, and high-risk and complex care management. Cano Health operates value-based primary care centers and supports affiliated medical practices that specialize in primary care for seniors in Florida, Texas, Nevada, and Puerto Rico, with additional markets in development. As part of its care coordination strategy, Cano Health provides sophisticated, high-touch population health management programs including telehealth, prescription home delivery, wellness programs, the transition of care, and high-risk and complex care management. The Company’s personalized patient care and proactive approach to wellness and preventive care set it apart from competitors. Cano Health has consistently improved clinical outcomes while reducing costs, affording patients the opportunity to lead longer and healthier lives. Cano serves a predominantly minority population (80% of its patients are Latino or African American) and a low-income population (50% of its patients are dual-eligible for Medicare and Medicaid).

Richard B. Aguilar, MD, is the Chief Clinical Officer for Cano Health and maintains his private practice with offices in Downey and Huntington Park, CA. Dr. Aguilar earned his medical degree at the University of California, Irvine College of Medicine, and completed his internship and residency in Internal Medicine at UC Irvine Medical Center and Long Beach Veterans Administration Medical Center. Dr. Aguilar is a member of the American College of PhysicianHe has served as Chief of Medicine and Chief of the ICU at several hospitals and from 2006 to 2010 was also Director of Diabetes Care for High Lakes Health Care in Bes, National Hispanic Medical Association as well as the American Diabetic Association.

Dr. Marlow Hernandez is the Chief Executive Officer of Cano Health and serves on its Board of Directors. Under Hernandez’s leadership, Cano Health has become one of the fastest-growing and most respected healthcare companies in Florida abiding by cultural attributes, which stand on the principles of always placing the needs of patients above all else; while striving to create a better and sustainable health care model to improve the lives of all Americans. Hernandez began practicing medicine in Pembroke Pines, FL alongside his family’s dental practice. Practicing medicine, running the medical business, while also taking on the task of night and weekend duties at local hospitals, Hernandez became one of the most accomplished medical professionals in the state before reaching the age of 30.

Opinion: Hernandez and Aguilar are forces of nature. I won’t bet against them. And it’s a SPAC, one of the few that are trading higher than its $10 nominal price.

November of last year Cano Health said it would go public by merging with Jaws Acquisition, (JWS) – Get Jaws Acquisition Report a special purpose acquisition company backed by real estate investor Barry Sternlicht, in a deal valued at $4.4 billion, including debt.The combined company will operate as Cano Health and will be listed on the New York Stock Exchange under the ticker symbol CANO.

Sternlicht is co-founder, chairman and chief executive of Starwood Capital Group, an investment fund with more than $60 billion of assets under management. He is also chairman of Starwood Property Trust and will be a board member.

As part of the transaction, Cano Health will receive an $800 million investment from investors including Sternlicht as well as funds related to and managed by Fidelity Management, BlackRock.

That’s the problem with these SPACs. There is an implied overhang from the SPAC sponsors. They can drop a stock bomb on you at any time but Hernandez and Aguilar must have known this was coming when they bought all these shares. . Cano Health filed to sell 75.3 M shares of common stock for holders on August 12th, the day they reported Q2 numbers and raised guidance only to lay a goose egg with the SPAC share dump. Q2 membership numbers increased by north of 50% year over year.

Apparently, the CEO and CFO are not worried about the share sale but it’s my job to worry. So maybe it doesn’t matter? Tell that to the Joby shareholders down 12% on Friday. Anyway, we made a fast 15% on our money with CANO and I’d like to buy more- once there is some clarity on the sponsor overhang. It is very possible that CANO can fulfill its mission to be the #1 primary care provider in America.

Name: Welch Joshua G

Position: Director

Shares Bought: 2,539, Average Price Paid: $124.75, Cost: $316,740

Company: Americas Carmart Inc. (CRMT)

America’s Car-Mart, Inc. operates automotive dealerships in twelve states and is one of the largest publicly held automotive retailers in the United States focused exclusively on the ‘Integrated Auto Sales and Finance’ segment of the used car market. The Company emphasizes superior customer service and the building of strong personal relationships with its customers. The Company operates its dealerships primarily in smaller cities throughout the South-Central United States selling quality used vehicles and providing financing for substantially all of its customers. America’s Car-Mart, Inc. is an ‘Integrated Auto Sales and Finance’ company also known as a ‘Buy Here Pay Here’ company. This means you can purchase, finance, and make payments directly to them– with no need for separate approvals. They sell quality, used vehicles, provide the financing and service the loan all right here at America’s Car-Mart. At Car-Mart, their associates deliver a customer experience centered around you – the customer and they will work with you one-on-one. Their purpose is to keep you on the road! They understand that buying a used vehicle is stressful and one of the biggest financial commitments someone might make during a lifetime. They are committed to helping you throughout the life of your financing term.

Joshua G. Welch serves as Independent Director of the Company. He currently serves as chairman of the compliance committee and a member of the audit, compensation, and nominating committees of our board of directors. Mr. Welch is the founder and currently the Managing Partner of Vicuna Capital I, LP, an investment management partnership founded in 1998. From June 1990 to June 1998, Mr. Welch was a securities analyst with the Tisch Family Interests, where he served on the board of Equimark Corp, then a publicly traded national bank. Mr. Welch is a graduate of Williams College and Columbia Business School and has served on numerous charitable boards. Mr. Welch’s qualifications to serve on the board include his financial and analytical skills.

Opinion: It looked like things were humming along at Car-Mart then the bottom fell out on the quarterly earnings report. Bank of America analyst just the prior month had upgraded it with a $165 target. Everyone knows used cars have skyrocketed and dealers are short on autos because the car manufactures can’t get enough semiconductors and have shut down assembly lines. Everything runs on semis- which makes us wonder why do we even need cars? aren’t we supposed to be in the metaverse anyway?

August 17th CRMT report Q2 EPS of $3.57 versus consensus $3.49 and same-store sales growth of 46.7%. Same-store sales were kinda meaningless since the prior years most car lots were closed down over the Covid pandemic. Total customers only grew by 3% since the beginning of the year. Panic set in that this was as good as it will get and the stock plummeted nearly $40 where director Welch stepped up and arrested the slide temporarily with his purchase at $124.75. Judging by his CV, Welch knows his shit and a stock trading now at a forward P.E of 9 looks cheap. CRMT has also been buying stock back and decreased the float.

I do believe the market is right taking a breather though, as 2020 comps are meaningless. What is the valuation based on 2019 earnings since they are not significantly growing customers at just 3%? On that metric looking at a more normalized going forward P.E, it seems like $8 earnings per share is doable and the multiple might be closer to 18 than 9

Name: Wells David B

Position: David

Shares Bought: 360,000, Average Price Paid: $8.24, Cost: $2,965,191

Company: Hims & Hers Health Inc. (HIMS)

Hims & Hers Health, Inc. is an American telehealth company that sells prescription and over-the-counter drugs online, as well as personal care products. The company is best known for selling generic treatments for erectile dysfunction and hair loss. Founded in 2017, it reached a valuation of $1.6 billion after closing a deal with Oaktree Capital Management to go public. Hims & Hers Health, Inc. operates a multi-specialty telehealth platform that connects consumers to licensed healthcare professionals. The company offers a range of health and wellness products and services available for purchase on its websites directly by customers. It provides prescription medication on a recurring basis and ongoing care from healthcare providers; and over-the-counter drug and device products, as well as cosmetics and supplement products, primarily focusing on wellness, sexual health, skincare, and hair care. The company’s curated non-prescription products include vitamin C, melatonin, collagen protein, biotin, and teas in the wellness category; moisturizer, fragrances, face wash, and anti-wrinkle creams in the skincare category; condoms and lubricants in the sexual health category; and shampoos, conditioners, scalp scrubs, and topical treatments, such as minoxidil in the hair care category. It also offers medical consultation services and engages in the wholesale of non-prescription product sales to retailers. Hims & Hers Health, Inc. is based in San Francisco, California. Hims and Hers offer online consultation to get prescriptions. The platform connects clients to doctors who prescribe the drugs based on an online intake form and photographs. The company also offers prescriptions for off-label uses, such as antidepressant sertraline for premature ejaculation. Some experts have expressed concerns about the safety of this process

David Wells brings a host of relevant experience as one of His & Hers’ newest Board of Directors members — including 15 years at the helm of Netflix’s finance team, most recently serving as its Chief Financial Officer. His experience working within rapid growth environments, as well as his understanding of the market and economy of industries, will help ensure the company’s growth is matched with an enduring, long-term business model. David is expected to serve as Chair of the Audit Committee for His & Hers Health, Inc.

Opinion: I’m not sure what to think of this Viagra seller and neither does the market. This is a large buy by David Wells and his first since being elected to the board in November 2020. This is another crappy SPAC deal born of the merger between digital health startup Hims and Hers and Oaktree investment partners back in January of 2021. The stock traded as high as $25.45 at the beginning of February, and has steadly rollled over.

Hims and Hers was orginally geared toward selling over the Internet easy to get prescriptions and drugs for erectile dysfunction and hair loss. In the past three years the company added a women’s health division, an online pharmacy and its own EHR. The best summary I’ve seen has been this article in healthcaredive.com

The Company’s goal is to become as a telehealth platform connecting uninsured consumers for a flat fee of around $20 a month for access to unlimited online consultations and a supply of generic medications.

Hims & Hers markets itself as a one-stop-shop for consumers, allowing them to bypass the traditional in-person care delivery pathway. It can be more expensive than other telehealth offerings but is still generally cheaper than the unbundled price of a doctor’s visit and full-price prescription, according to SVB Leerink analyst Stephanie Davis.

The company has seen rapid growth. Since its launch a little more than three years ago, Hims & Hers has run more than 2 million telehealth visits and seen 100% compounded annual revenue growth, from $27 million in 2018 to $83 million in 2019 and an expected $138 million this year, per internal data. The company is not profitable and the $317 million cash on its books might not be enough in the ground turf war healthcare is.

Hims & Hers has more than doubled gross margins to 71%, with recurring revenue making up 91% of its top line. However, the company has yet to turn a profit and doesn’t expect that to change in the near term as it reinvests in growth, according to financial documents filed with the SEC in December.

According to healthcaredive.com, “beyond growing pains, Hims & Hers also faces additional risk as it looks to scale in the increasingly crowded and rapidly evolving virtual care market, elbowing against telehealth giants like Teladoc and Amwell and technology behemoths and retail pharmacies interested in the lucrative space, such as Amazon and CVS Health.

Name: Sadun Raffaele

Position: CFO

Shares Bought: 95,000, Average Price Paid: $8.90, Cost: $845,500

Name: Grant William Thomas

Position: COO

Shares Bought: 230,000, Average Price Paid: $8.85, Cost: $2,035,500

Name: Grant Robert Clay

Position: President

Shares Bought: 230,000, Average Price Paid: $8.79, Cost: $2,021,700

Name: Danker Timothy Robert

Position: CEO

Shares Bought: 117,000, Average Price Paid: $8.75, Cost: $2,965,191

Company: SelectQuote Inc. (SLQT)

Founded in 1985, SelectQuote (NYSE: SLQT) provides solutions that help consumers protect their most valuable assets: their families, health, and property. The company pioneered the direct-to-consumer model of providing unbiased comparisons from multiple, highly-rated insurance companies allowing consumers to choose the policy and terms that best meet their unique needs. Two foundational pillars underpin SelectQuote’s success: a strong force of highly-trained and skilled agents who provide a consultative needs analysis for every consumer, and proprietary technology that sources, scores, and routes high-quality sales leads. The company has three core business lines: SelectQuote Senior, SelectQuote Life, and SelectQuote Auto and Home. SelectQuote Senior, the largest and fastest-growing business, serves the needs of a demographic that sees 10,000 people turn 65 each day with a range of Medicare Advantage and Medicare Supplement plans from leading, nationally recognized carriers, as well as prescription drug plans, dental, vision and hearing plans. SelectQuote, Inc. is a technology-enabled, direct-to-consumer distribution platform that provides consumers with a transparent and convenient venue to shop for complex senior health, life, and auto & home insurance policies from a curated panel of insurance carriers. The company operates through three business lines: SelectQuote Senior, SelectQuote Life, and SelectQuote Auto & Home. The SelectQuote Senior provides unbiased comparison shopping for Medicare Advantage and Medicare Supplement insurance plans as well as prescription drug plans, dental, vision and hearing, and critical illness products. SelectQuote Life provides unbiased comparison shopping for life insurance and ancillary products including term life, guaranteed issue, final expense, accidental death, and juvenile insurance. The SelectQuote Auto & Home provides an unbiased comparison shopping platform for auto, home, and specialty insurance lines.

Opinion: Although these are large buys by the above insiders, it’s important to keep things in perspective. They’ve sold so much SLQT stock in the past that these most recent buys at these very depressed prices are almost a free toss of the coin. They are all very highly paid executives who have a vested interest in keeping their jobs and showing support for the company.

Name: Armstrong Timothy M

Position: Director

Shares Bought: 9,000, Average Price Paid: $7.61, Cost: $68,490

Name: Adelman David J

Position: Director

Shares Bought: 100,000, Average Price Paid: $7.54, Cost: $754,000

Company: Wheels Up Experience Inc. (UP)

Wheels Up is an aviation company that primarily serves members in the United States. In 2013, Kenny Dichter, Bill Allard, and Justin Firestone, it was founded using a membership/on-demand business model. Wheels Up Experience Inc. provides private aviation services primarily in the United States. The company offers a suite of products and services, including multi-tiered membership programs, on-demand flights across various private aircraft cabin categories, aircraft management, retail and wholesale charter, whole aircraft acquisitions and sales, corporate flight solutions, special missions, signature events and experiences, and commercial travel. It operates a fleet of approximately 1,500 owned, leased, managed, and third-party aircraft. The company was founded in 2013 and is headquartered in New York, New York. Using a mobile application, Wheels Up members can book short- and medium-range private planes from the company fleet at an all-inclusive hourly rate. It differs from competitors such as NetJets, where members own shares of specific aircraft and, according to Time, is more like on-demand rental systems like Zipcar. Following its acquisitions of Delta Private Jets, Travel Management Company, and Gama Aviation Signature, Wheels Up Group is now the second-largest private aircraft operator in the U.S. behind NetJets, with 160,161 flight hours in 2019 3.6% of the U.S. Part 91, 91K and 135 markets.

Mr. Armstrong has served as a member of the board of directors of WUP since April 2019. Mr. Armstrong is the Founder and Chief Executive Officer of the Flowcode/dtx company, a direct-to-consumer enablement company he established in February 2019. From March 2009 to September 2018, Mr. Armstrong served as the Chair and Chief Executive Officer of AOL and the Chief Executive Officer of Oath (Verizon’s media brand portfolio, which included Yahoo! and AOL) after Verizon acquired AOL in May 2015. From 2000 to 2009, They believe Mr. Armstrong is well qualified to serve on the board of directors of Wheels Up due to his extensive executive leadership experience, his expertise concerning marketing and sales, particularly with digital/online products, as well as his prior service as a member of executive leadership teams and boards of directors of public companies, along with his service as a member of the board of directors of WUP since 2019.

Mr. Adelman has served as a member of the board of directors of WUP since October 2013. Mr. Adelman is a Philadelphia-based entrepreneur and active private investor. He is the co-founder and has served as the Vice-Chairman of FS Investments, a leading manager of alternative investment funds with $24 billion of assets under management, since December 2007. Mr. Adelman has also served as the Chief Executive Officer of Campus Apartments, a Philadelphia-founded firm that he built into a national leader in student housing development and management, with more than $2 billion in assets under management across 17 states in 1997. They believe he is well qualified to serve on the board of directors of Wheels Up due to his entrepreneurial success, extensive investment experience, and service as a member of the board of directors of WUP since it was founded and numerous other companies.

Opinion: It’s just another crappy SPAC offering. I have no problem with greed but lots of unproven business models have gone public prematurely with the SPAC revolution. It’s almost the natural reaction to the Airbnb’s and Ubers that waited too long to go public leaving the public shareholders with mature companies that insiders and VCs have picked clean. In the case of Wheels UP, it sounds like it’s almost Uber for jets. Even Uber has yet to make any money.

Follow us on Twitter for real-time insider buying alerts at https://twitter.com/theinsidersfund.

[custom-twitter-feeds]

Insiders sell the stock for many reasons, but they generally buy for just one – to make money. You’ve always heard the best information is inside information. Everyone who has any experience at all in the stock market pays close attention to what insiders are doing. After all, who knows a business better than the people running it? Officers, directors, and 10% owners are required to inform the public through a Form 4 Filing any transaction, buy, sell, exercise, or any other with 48 hours of doing so. This info is available for free from the SEC’s Web site, Edgar, although we subscribe to SECForm4 as they provide a way to manage and make sense of the vast realms of data. I’ve tried many vendors, and SECForm4 is one of the most customer-friendly and responsive I’ve used.

We publish a subscription newsletter called The Insiders Report. We offer a free 30-day trial, so you have nothing to lose by trying it out. Be sure to carefully read the TERMS OF SERVICE.

Another source for insider buying and selling and much more is FinViz Elite. FinViz stands for financial visualization, and they do an amazing job of providing reams of data and the tools to help you get to the bottom of it, the information that helps me make informed decisions and probable outcomes. I’ve been using their site for years, and it only gets better over time.

This is as close to “insider information” that an ordinary investor is likely to see- and it’s entirely legal.

BEWARE– Following insiders can be hazardous to your financial health unless you know what you are doing. Unlike the raw, unfiltered data, The Insiders Fund blog informs you of the purchases that count, the ones that are just window dressing into deceiving the public that all is hunky-dory, and those that are just flat out other people’s money and should be just discarded like bad fish. As a rule, we only look at material amounts of money, $200 thousand or more, as anything less could just be window dressing.

The bar is different from selling because the natural state of management is to be sellers. This is because most companies provide significant amounts of management compensation packages as stock and options. Therefore, with selling, we analyze for unusual patterns, such as insiders selling 25 percent or more of their holdings or multiple insiders selling near 52-week lows. Another red flag is large planned sale programs that start without warning. Unfortunately, the public information disclosure requirements about these programs referred to as Rule 10b5-1 are horrendously poor. Also, planned sales that just pop up out of nowhere are basically sales and are seeking cover under the Sarbanes Oxley corporate welfare clause. I also generally ignore 10 percent shareholders as they tend to be OPM (other people’s money) and perhaps not the smart money we are trying to read the tea leaves on.

Of course, insiders can also be wrong about their Company’s prospects. Don’t let anyone fool you into believing they never make mistakes. No one tracks and understands insider behavior better than us. We’ve been doing it religiously since 2001 when I quit being an insider myself and devoted myself full time to managing my personal investments. They can easily be wrong about how much others will value them, and in many cases, maybe most cases have no more idea what the future may hold than you or me. In short, you can lose money following them. We have, and we curse aloud, what were they thinking! Needless to say, past good fortune is no guarantee of future success. We may own positions, long or short, in any of these names and are under no obligation to disclose that. We welcome your comments on our analysis.

That’s where analysis comes in. Know what you own. Eventually, you will wish you did this so I’m making it easy for you to get on it. Use my guide Stock Checklist- my Perfect 10 or create your own but do your research. Besides being the single most important document to read about a company, this is the annual report and it is required by all public companies to file. Every word is read over, picked over, and circulated amongst the CEO, the CFO, the inside counsel, the outside counsel, and the auditors before its filing. On top of it, the CFO and/or CEO have to swear under oath that it’s truthful to the best of their knowledge. Everything else could be full of fluff and as insightful as a basketball coach at halftime rallying his team that’s 20 points behind with no chance of winning.

Two more insightful and affordable sources I use every day or The Fly on the Wall and Briefing. Together they make my poor man’s Bloomberg and are faster and easier for me to whirl around.

This blog is solely for educational purposes and the author’s own amusement. Investing with The Insiders Fund is for qualified investors and by Prospectus only. Nothing herein should be construed otherwise. THE INSIDERS FUND invests in companies at or near prices that management has been willing to invest significant amounts of their own money in. If you would like to hear more about how you can get involved with the Insiders Fund, please schedule some time on my calendar.

Prosperous Trading,

Harvey Sax

The Insiders Fund was the 4th best long-short equity fund in the world in 2019, 4th Best in November 2020, 4th Best in January 2021 (I kid you not)