For trade, details click on this link to the trades

A few names from last week’s insider buys stand out. Insider buying/selling ratios are improving a bit as well. We are always on the lookout for beaten-up sectors in the market that start attracting insider buying. Last year between June and September regional bank insiders were buying their shares hand over fist. That turned out to be one of the best buying opportunities in this beaten-down sector. The regional bank ETF KRE has beaten the S&P 500 by nearly 50% points during the last year.

Last week we see two names in the renewable and alternative energy space, and three development-stage biotechs. The alternative energy sector ran up dramatically on the promise of a New Green Deal on Biden’s election but the reality of working with a divided Congress has begun to set in. Now it’s questionable if anything significant will really get done toward a greener future from our elected representatives. There is no question in my mind, though, that the private sector and the reality of global warming will force the issue.

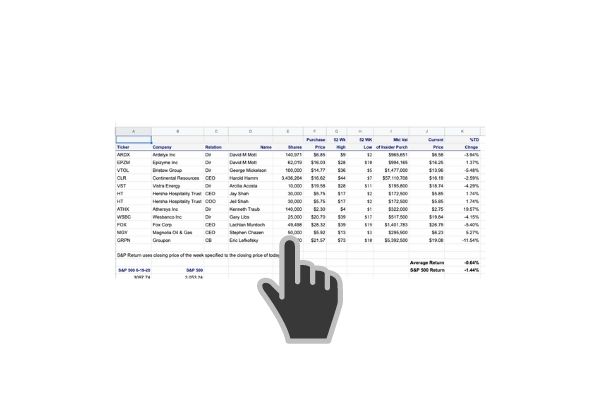

Jeffrey Immelt, former General Electric, CEO, and now a board member of Bloom Energy purchased 38,000 shares at $19.82. Bloom was everyone’s darling last year. Bloom Energy is a public company headquartered in San Jose, California. It manufactures and markets solid oxide fuel cells that produce electricity on-site. The company was founded in 2001 and came out of stealth mode in 2010. It raised more than $1 billion in venture capital funding before going public in 2018. Wikipedia We are buying BE.

We’re familiar with Pacific Ethanol but it changed its name to Alto Ingredients. They just sold a fuel ethanol facility to Seaboard Energy and that shored up its balance sheet. After the close, the company’s outstanding balance of its senior notes was under $1 million. Alto Ingredients, Inc. (ALTO), formerly known as Pacific Ethanol, Inc., is a leading producer of specialty alcohols and essential ingredients. The company is focused on products for four key markets: Health, Home & Beauty; Food & Beverage; Essential Ingredients; and Renewable Fuels. The company’s customers include major food and beverage companies and consumer products companies. For more information please visit www.altoingredients.com.

I like where Alto is headed. According to the CEO on May 12th, “We had a solid first quarter to start 2021. Sales of our specialty alcohols came from contracted volumes, spot sales and exports. We generated our fourth consecutive quarter of gross profit and had a net income of $4.4 million and adjusted EBITDA of $13.6 million in the first quarter. CEOs are notorious cheerleaders and outright scoundrels on earnings call as they had behind the safe harbor provisions and make outrageous claims and predictions. It’s only when management backs it up with their own money, do I take much stock in it. Director Nahan purchased 79,659 shares of ALTO at $5.56.

ALTO is an inexpensive play on the growth of renewables. We now own it again but don’t expect the repeat performance when it nearly doubled last year on an insider buy. We blogged about it last August and made good money on it. too. Now that the stock price has round-tripped almost back to where we got invested the first time,

The transaction with Basanite is a private market transaction and should basically be discarded. The reason I didn’t do just that is that Basanite is actually a pretty interesting publicly traded startup. From the most recent 10K- (by the way this is the first place after the company website, that any investor should go when researching a stock. On May 30, 2006, Basanite, Inc. was organized as a Nevada corporation. Basanite and its wholly-owned subsidiaries are herein referred to as the “Company”, “we”, “our”, or “us”. Currently based in Pompano Beach, Florida, the Company manufactures concrete-reinforcing products made from basalt fiber reinforced polymers (“BFRP”), such as its primary product BasaFlexTM. This UV-stable, chemical, acid and moisture resistant material is sustainable and environmentally friendly and has been engineered to replace steel as it never rusts, therefore, addressing the industry’s current corrosion issue.

As far as K’s go, this is definitely a colorful one. THERE IS NO INVESTMENT OPPORTUNITY HERE. Although basalt rebar is a substitute for steel-reinforced concrete looks like a timely idea, this company is not the only one making it. In fact, it’s not the inventor or even presently can manufacture it, as far as I can tell, and has no financial resources to compete in this market. Like everything else, you can buy it on Amazon. But it does bring up an interesting idea that I want to research further. With the moment growing to spend massive amounts of money o aging bridges, tunnels, and infrastructure– this area looks ripe for investment if you can find that right horse to ride. It doesn’t look like this horse has left the barn yet as basalt rebar is not approved in most or for that matter may be any building codes. That could change and if costs, demand, and complexity of manufacturing get to the point where it will be a big business, you can expect Dupont or somebody big in the composite business to be all over it. Since basalt is a naturally occurring rock, one of the most common in the world, it’s hard to see any patent game here either.

RadNet is the largest provider of freestanding, fixed-site outpatient diagnostic imaging in the country with more than 330 centers. Everyone knows that Covid put a backseat on a lot of medical procedures. Certainly, there is pent-up demand but beyond this is there a great runway? I don’t know the answer to that but Director Levitt purchased 12,500 shares of RDNT at $23.07. It’s curious though as he sold 20,000 shares at $23.07 back in March. I don’t know what to make of it but there are no other insiders buying so we’re moving on.

Perhaps by now, you’ve been to the mall or out shopping in the real world? Have you been to the Container Store? The Container Store Group, Inc. is an American specialty retail chain company that operates The Container Store, which offers storage and organization products, and custom closets. The company has made Fortune’s list of “100 Best Companies to Work For” in each of the past 17 years, through 2016. Wikipedia

Here’s the kicker. Everyone is talking about the phenomenon of soaring house values and bidding wars. HomeDepot, Lowers, and home builders stocks are at record highs but TCS is just barely above its 2020 year-end price. The Container Store blew the doors off Q4 earnings on May 18th and the stock jumped 4% to $13.60. Then on the earnings call they said they see revenue up 50% from last year’s easy but gross margins would contract in FY21 because of higher commodity costs, freight, and shipping headwinds. and the stock dropped 11.7% the next day. CEO Malhotra just bought 20,500 shares at $12.25. TCS is a decent value perhaps even a foot-stomping good value here at 11.56 x trailing 12-month earnings and just 5.59 X free cash flow. They have a decent balance sheet too. We will likely be buyers of this name on Monday.

Director Ferraioli bought 10,000 shares of Vistra at $15.94-$16.00. This is a good value on our favorite theme right now. We’ve been telling anyone who will listen to us that this is a big opportunity. We focused on the game-changing opportunity electric utility companies have in our post on May 16th . We’d buy more if VST wasn’t already The Insiders Fund’s largest position followed by Avangrid, another utility.

Insiders are adding to their holdings into Garrett Motion, GTX. We have a small position in this name but are growing more interested as insiders buying post-bankruptcy continues. This was highlighted in last week’s blog post. CEO Olivier added 25,000 shares of GTX at $6.60.

Three development stage biotechs hit up our screens. Chief Scientific Officer, Arthur Krieg bought 25,0001 shares of Checkmate Pharmaceuticals at $6.97. He has been buying CMPI since 12-17-20 at $14.62 per share. Although the purchases are not large he keeps adding to his money-losing position. That’s a strong conviction. Checkmate Pharmaceuticals is a clinical-stage biopharmaceutical company focused upon activation of innate immunity to treat cancer.

Peter A. Cohen is certainly as sophisticated an investor as you can find, as former head of Shearson Lehman Hutton, which a the time was the largest brokerage firm in the U.S. Mr. Cohen purchased 265,000 shares of PTE at $.98 per share. PTE has been around for some time. Its founders Lough and Swanson left coveted Plastic Surgery resident positions to become the CEO and COO of Majesco Entertainment Co. (Nasdaq: COOL) in hopes that a merger between a 31-year-old failing gaming company and their own revolutionary technology would provide the field of medicine with the ability to regenerate new tissue — skin, bone, muscle, etc. Lough and Swanson are taking a huge gamble because the culture in the medical community is that you don’t leave to try a start-up and then come back if it doesn’t work. The result was Polarity Te. Forbes wrote an article on it on August 17th, Polarity TE: Will this Biotech be the next Amazon or Tesla?

Mr. Cohen can certainly afford to lose his investment in Polarity TE so without any other less fortunate insiders buying this name, we are not playing in this sandbox. I do think we would get terribly interested if Dr. Swanson purchased a significant amount in the open market.

It’s always encouraging when insiders buy their own company’s stock. In the field of bioscience where the outcomes are often binary and nearly impossible for the average investor to predict, insider behavior analysis is the closest thing you got to unblinding the drug trials themselves. It’s promising when the Chief Scientific Officer is the insider doing the buying.

General counsel Schundler purchased 97,755 shares of Liquidia Corp at $2.77 per share. Liquidia is a biopharmaceutical company focused on the development and commercialization of products that address unmet patient needs, with a current focus directed towards the treatment of pulmonary arterial hypertension (PAH). LQDA has a big investor, Eshelman Ventures, sitting on the stock selling significant amounts in January which undoubtedly weighed on the share price. When the general counsel is buying the first thing I think of is M&A or patent litigation. When I searched the most recent 10K on legal or patents, not much stood out except for their current patent litigation with United Therapeutics. The company announced on May 10th that they are resubmitting their NDA for their LIQ861 drug for the treatment of pulmonary arterial hypertension in response to the FDA’s initial complete response rejection back in November 2020. They recently concluded a private placement and a merger with a company, RareGen, in preparation for sales into the PAH market.

This litigation is a very big deal. United Therapeutics has initiated a lawsuit against the Company in which it claims that LIQ861 is infringing three of its patents, which may result in our company being delayed in its efforts to commercialize LIQ861. The bottom line, the general counsel is betting on a favorable outcome to litigation. That’s the only logical explanation. This is way too complicated and binary for us so we are on the sidelines.

Director Kramer bought 40,000 shares of Option Care Health, Inc. at $17.59. Option Care Health is the nation’s largest independent provider of home and alternate-site infusion services. With over 5,000 teammates, including approximately 2,900 clinicians, we work compassionately to elevate standards of care for patients with acute and chronic conditions in all 50 states. I’m having a hard time seeing anything to get excited about with OPCH.

Follow us on Twitter for real time insider buying alerts at https://twitter.com/theinsidersfund

[custom-twitter-feeds]

Insiders sell stock for many reasons, but they generally buy for just one – to make money. You’ve always heard the best information is inside information. Everyone who has any experience at all in the stock market pays close attention to what insiders are doing. After all, who knows a business better than the people running it? Officers, directors, and 10% owners are required to inform the public through a Form 4 Filing any transaction, buy, sell, exercise, or any other with 48 hours of doing so. This info is available for free from the SEC’s Web site, Edgar, although we subscribe to SECForm4 as they provide a way to manage and make sense of the vast realms of data. I’ve tried a lot of vendors and SECForm4 is one of the most customer-friendly and responsive I’ve used.

We publish a subscription newsletter called The Insiders Report. We offer a free 30-day trial so you have nothing to lose by trying it out. Be sure to carefully read the TERMS OF SERVICE.

Another source for insider buying and selling and much more is FinViz Elite. FinViz stands for financial visualization and they do an amazing job of providing reams of data and the tools to help you get to the bottom of it, the information that helps me make informed decisions and probable outcomes. I’ve been using their site for years and it only gets better over time.

This is as close to “insider information” that an ordinary investor is likely to see- and it’s entirely legal.

BEWARE– Following insiders can be hazardous to your financial health unless you know what you are doing. Unlike the raw, unfiltered data, The Insiders Fund blog informs you of the purchases that count, the ones that are just window dressing into deceiving the public that all is hunky-dory, and those that are just flat out other people’s money and should be just discarded like bad fish. As a rule, we only look at material amounts of money, $200 thousand or more, as anything less could just be window dressing.

The bar is different from selling because the natural state of management is to be sellers. This is because most companies provide significant amounts of management compensation packages as stock and options. Therefore, with selling, we analyze for unusual patterns, such as insiders selling 25 percent or more of their holdings or multiple insiders selling near 52-week lows. Another red flag is large planned sale programs that start without warning. Unfortunately, the public information disclosure requirements about these programs referred to as Rule 10b5-1 is horrendously poor. Also planned sales that just pop up out of nowhere are basically sales and are seeking cover under the Sarbanes Oxley corporate welfare clause. I also generally ignore 10 percent shareholders as they tend to be OPM (other people’s money) and perhaps not the smart money we are trying to read the tea leaves on.

Of course, insiders can also be wrong about their Company’s prospects. Don’t let anyone fool you into believing they never make mistakes. No one tracks and understands insider behavior better than us. We’ve been doing it religiously since 2001 when I quit being an insider myself and devoted myself full time to managing my personal investments. They can easily be wrong about how much others will value them, and in many cases, maybe most cases have no more idea what the future may hold than you or I. In short, you can lose money following them. We have and we curse aloud, what were they thinking! Needless to say, past good fortune is no guarantee of future success. We may own positions, long or short, in any of these names and are under no obligation to disclose that. We welcome your comments on our analysis.

This blog is solely for educational purposes and the author’s own amusement. Investing with The Insiders Fund is for qualified investors and by Prospectus only. Nothing herein should be construed otherwise. THE INSIDERS FUND invests in companies at or near prices that management has been willing to invest significant amounts of their own money in. If you would like to hear more about how you can get involved with the Insiders Fund, please schedule some time on my calendar.

Prosperous Trading,

Harvey Sax

The Insiders Fund was the 4th best long-short equity fund in the world in 2019, 4th Best in November 2020, 4th Best in January 2021 (I kid you not)