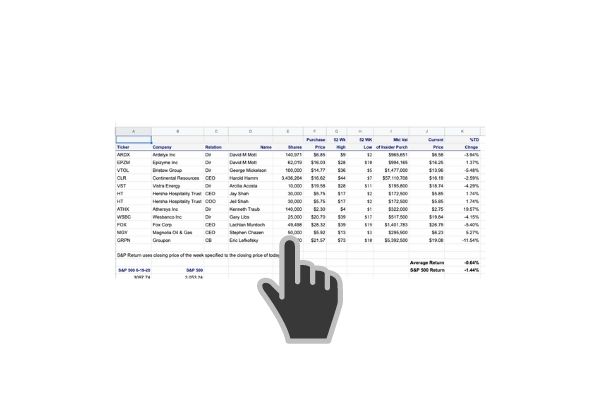

For trade details click on this link to the trades

insider-trading/1691077.htm”>Rideshare Rental Inc. up 42.61%

Allied Esports Entertainment Inc. up 25.63%

STEEL PARTNERS HOLDINGS L.P. up 21.51%

ENERGY INC"}” data-sheets-userformat=”{"2":8193,"3":{"1":0},"16":8}” data-sheets-hyperlink=”https://www.secform4.com/insider-trading/886128.htm”>FUELCELL ENERGY INC up 15.40%

PIMCO Dynamic Income Opportunities Fund up 1.65%

INTEL CORP up 0.31%

PIMCO Flexible Municipal Income Fund up 0.09%

B. Riley Financial Inc. down -0.68%

TEMPLETON GLOBAL INCOME FUND down 0.71%

TELEDYNE TECHNOLOGIES INC down 2.47%

LANDEC CORP down -2.91%

Driven Brands Holdings Inc. down -5.67%

![]()

Rideshare Rental Inc. 10% owner, John Gray bought 412,040 shares at $1.54. Not a bad week for Mr. Gray, up on paper 42.61%. RideShare Rental provides drivers with aspirations to drive for Uber and Lyft the desired vehicles to do it with. Uber and Lyft are not very picky about who drives for them but they are about the cars you use. Get with the YAYO program and they do the rest providing Uber– and Lyft-approved vehicles on a daily, weekly, and monthly basis. Just use the RideShare Rental app or website to choose the car you want. RideShare Rental will handle all the paperwork and insurance so you can start earning right away. Sound like a crazy idea? Hertz is doing the same thing.

Allied Esports Entertainment Inc.

AESE deserves more attention and I will be skiing with my Gen Z son today and I’m going to be researching this one with him while shredding at Deer Valley.

CEO Few bought 11,000 shares of FuelCell Energy at $17.99. He’s up 15.40% for the week. The stock was $2 right before the election. Anything with a name like FuelCell exploded in price. It’s curious to see the CEO buying instead of selling. We’re kicking ourselves over missing this one as there was insider buying at $.75 as well. Who needs Tesla stock when you can rise 40x in the price? FuelCell Energy delivers efficient, affordable and clean solutions for the supply, recovery, and storage of energy. We design, manufacture, undertake project development, install, operate and maintain megawatt-scale fuel cell systems, serving utilities, industrial and large municipal power users with solutions that include both utility-scale and on-site power generation, carbon capture, local hydrogen production for transportation and industry, and long-duration energy storage. But wait, here’s the real kicker. FCEL has shrunk in revenues every year since 2016 except for 2020 where it grew to $70.87 Million, $10 million more than in 2019. Before you get too excited, FCEL has $108.25 million in revenues in 2016. Does this warrant this kind of price appreciation? I’m afraid the train has left the station although the CEO buying here might indicate otherwise. Few has been CEO since 2019 yet this is his first purchase now that the stock has risen twentyfold. He does appear to have a ton of employee restricted stock units (RSUs) so he doesn’t really need to buy some stock- or does he? Is this one of the games corporate CEO’s and Boards of Directors play? This is the kind of insider window dressing that annoys the heck out of me. Why pretend you have good corporate Governance when you put up sham transactions like buying a pittance of stock when you’ve been awarded millions of shares. Just come out and explain that you’re doing a little window dressing thinking that it might actually be a good thing if your CEO paid for some stock instead of just being handed buckets of it through the corporate RSU compensation plan.

Want to buy into a hedge fund. That’s what VP Gordon Walker did when he purchased 70,182 shares at $11.11 of STEEL PARTNERS HOLDINGS L.P.. I don’t know what the motives are but he’s up 21.51% for the week. Steel Partners seems to be on the mend, the stock more than doubling since last Summer but is only now back to its price in August 2019. You’re on your own with SPLP although we did have an intern that worked for us that has been at Web Bank for some time, an SPLP 100% owned company.

PIMCO Dynamic Income Opportunities Fund PDO Chief Investment Officer Ivascyn bought 250,000 shares at $20. We don’t normally pay much attention to fund managers investing in their own funds but in this case, there were many of Pimco’s employees buying into the fund, the largest being this $5 million purchase. Either this is a damn good fund, or PIMCO is way overpaying their employees. PDO is a newly launched fund with a lot of insider buying. According to PIMCO, the fund will normally invest at least 25% of its total assets in mortgage-related assets issued by government agencies or other governmental entities or by private originators or issuers. The fund may invest up to 30% of its total assets in securities and instruments that are economically tied to “emerging market” countries; however, the fund may invest without limitation in short-term investment-grade sovereign debt issued by emerging market issuers. The fund may normally invest up to 40% of its total assets in bank loans (including, among others, senior loans, delayed funding loans, covenant-lite obligations, revolving credit facilities, and loan participations and assignments). It is expected that the fund normally will have a short to intermediate average portfolio duration (i.e., within a zero to eight-year range), although it may be shorter or longer at any time depending on market conditions and other factors.

I don’t know what the yield is on this fund as I couldn’t find that on their website or even a casual look a the newly issued prospectus. I do know the expenses, though, and at 2.65%, that’s more than you can earn on some mortgage products in today’s low-interest-rate environment. Undoubtedly PIMCO will have to leverage the Fund heavily to get some yield, up to 50% and they can invest in junk bonds. This one should be interesting to watch as it will probably have a junk bond-like yield with a government back wrapper. I’d stay away from this one even with all the management buying in. These closed-end bonds funds usually trade at a discount to NAV and the high yield can quickly be lost in the drop in share price. Let it season before you dip your toe in the water here.

Intel, Intel, the gift that keeps on disappointing. We lost money trading Intel last quarter but we’re back at it again. Like a lot of people including Third Point’s Dan Loeb, we can’t believe America’s chip giant has sunken so low. There is a worldwide glut of chips- how can Intel have missed the wave by such a wide margin. The stock briefly rallied 8% after Third Point, an activist investor, announced a stake in the Company and called for a management shake-up. The stock rallied on this, only to disappoint once again when they released their earnings. That’s about when the CEO and CFO stepped up and bought some stock.

CFO Davis bought 9,095 shares at $55.34, roughly a half-million dollars worth and CEO Swan bought 27,244 shares at $55.57, a million and a half; basically a token investment at this point. I do believe like Loeb that something can be done with the Company. The off chance that China and the U.S squabble further about the independence of Tawain and thus Tawain Semi could cause INTC stock to leap skyward. Also, President Biden has something of a buy American message he is trying to lay down. Intel is the ultimate buy American chip company. I doubt if we are going to lose much money on buying Intel. Waiting for Intel to get their act together again is no longer an option with Third Point on their throat now. Expect some quick action, like Bob Swan, the CEO, doing a swan song exit soon.

CEO Riley keeps buying, buying, and buying brokerage company, B.Riley Financial. Business must be very good as it’s unusual for management to buy their stock at 52-week highs. Last week Riley bought 18,000 more shares of RILY at $48.53. Lots of good business momentum at this firm. Last week B. Riley Advisory Services named turnaround consulting firm of the year. B.Riley merged with FBR & Co in 2017 and has been pedal to the metal since.

B. Riley Financial, Inc. (NASDAQ: RILY) (“B. Riley” or the “Company”), a leading business advisory and financial services company, today announced it has adopted new brand names across its subsidiary companies to provide greater external consistency and affiliation among the diverse stakeholders it serves.

B. Riley has experienced meaningful growth since its founding in 1997 by co-Chief Executive Officers Bryant Riley and Tom Kelleher. The Company’s brand realignment follows the integration of a series of acquisitions B. Riley has completed since 2015 which include, among others, Friedman, Billings & Ramsey (FBR & Co.); GlassRatner; Great American Group; and Wunderlich Securities.

“The addition of these companies over the last five years has meaningfully transformed our B. Riley platform. As we look ahead to future growth, our goal is to drive greater visibility and awareness for the depth and breadth of B. Riley’s diverse suite of services and our ability to deliver end-to-end solutions to support our clients, partners and stakeholders,” said Bryant Riley, Chairman and co-Chief Executive Officer, B. Riley Financial.

![]()

Templeton Funds is best known for managing international investments so it makes sense to pay attention to when one of Wall Street’s savviest investors, Saba Capital Management, buys into Templeton Global Income Fund. Saba bought 924,941 shares of GIM at $5.63. Boaz Weinstein is a legendary investor, best known for his credit analysis, so an endorsement of GIM is worth paying attention to. The long term history of the Fund, though, is abysmal. The Fund aims to provide current income with a secondary goal of capital appreciation. Perhaps this secondary goal should be reevaluated as the Fund launched at $10 per share and is now trading for nearly half of that. The current yield on the Fund is about 3.20%

Chairman and CEO, Mehrabian, bought 10,000 shares of Teledyne Technologies at $366.05. TDY Teledyne Technologies Incorporated is an American industrial conglomerate. It was founded in 1960, as Teledyne, Inc., by Henry Singleton and George Kozmetsky. Robert Mehrabian has been the CEO since 1999. TDY has been an excellent long term hold and perhaps Mehrabian was taking advantage of a small dip in the share price after recent earnings. This is the CEO’s first purchase since June 1th of 2017 when he purchased 10,000 shares at $129.4. Since then he has sold quite a bit of stock but it all seems to be related to the exercise and sale of stock options. It must be nice to get stock options as part of your compensation. It makes it a lot harder to reach anything significant into the purchase when he has been a consistent seller.

VP Mendoza bought 30,000 shares of DRVN at $29.79 on 1-21 and Director, Puckett bought 15,000 shares at $28 on 1-14. Its very encouraging that executives are buying the stock up significantly after the IPO. Driven Brands is the largest automotive services company in North America, with a portfolio of highly recognizable brands( that fulfill an extensive range of consumer and commercial automotive needs, including paint, collision, glass, vehicle repair, oil change, maintenance, and car wash. The Company went public on Jan 15th at $22. They describe themselves on their Linkedin page as the quintessential growth company, more than tripling its revenues, brands, employees, and profits over the past six years. But are they really? Much of the process of the IPO went to pay off some of the debt binged growth and the P.E company behind it, including its August 2020 purchase of International Car Wash Group.

Follow us on Twitter for real time insider buying alerts at https://twitter.com/theinsidersfund

[custom-twitter-feeds]

Insiders sell stock for many reasons, but they generally buy for just one – to make money. You’ve always heard the best information is inside information. Everyone who has any experience at all in the stock market pays close attention to what insiders are doing. After all, who knows a business better than the people running it? Officers, directors, and 10% owners are required to inform the public through a Form 4 Filing any transaction, buy, sell, exercise, or any other with 48 hours of doing so. This info is available for free from the SEC’s Web site, Edgar, although we subscribe to SECForm4 as they provide a way to manage and make sense of the vast realms of data. I’ve tried a lot of vendors and SECForm4 is one of the most customer-friendly and responsive I’ve used.

Another source for insider buying and selling and much more is FinViz Elite. FinViz stands for financial visualization and they do an amazing job of providing reams of data and the tools to help you get to the bottom of it, the information that helps me make informed decisions and probable outcomes. I’ve been using their site for years and it only gets better over time.

This is as close to “insider information” that an ordinary investor is likely to see- and it’s entirely legal.

BEWARE– Following insiders can be hazardous to your financial health unless you know what you are doing. Unlike the raw, unfiltered data, The Insiders Fund blog informs you of the purchases that count, the ones that are just window dressing into deceiving the public that all is hunky-dory, and those that are just flat out other people’s money and should be just discarded like bad fish. As a rule, we only look at material amounts of money, $200 thousand or more, as anything less could just be window dressing.

The bar is different from selling because the natural state of management is to be sellers. This is because most companies provide significant amounts of management compensation packages as stock and options. Therefore, with selling, we analyze for unusual patterns, such as insiders selling 25 percent or more of their holdings or multiple insiders selling near 52-week lows. Another red flag is large planned sale programs that start without warning. Unfortunately, the public information disclosure requirements about these programs referred to as Rule 10b5-1 is horrendously poor. Also planned sales that just pop up out of nowhere are basically sales and are seeking cover under the Sarbanes Oxley corporate welfare clause. I also generally ignore 10 percent shareholders as they tend to be OPM (other people’s money) and perhaps not the smart money we are trying to read the tea leaves on.

Of course, insiders can also be wrong about their Company’s prospects. Don’t let anyone fool you into believing they never make mistakes. No one tracks and understands insider behavior better than us. We’ve been doing it religiously since 2001 when I quit being an insider myself and devoted myself full time to managing my personal investments. They can easily be wrong about how much others will value them, and in many cases, maybe most cases have no more idea what the future may hold than you or I. In short, you can lose money following them. We have and we curse aloud, what were they thinking! Needless to say, past good fortune is no guarantee of future success. We may own positions, long or short, in any of these names and are under no obligation to disclose that. We welcome your comments on our analysis.

This blog is solely for educational purposes and the author’s own amusement. Investing with The Insiders Fund is for qualified investors and by Prospectus only. Nothing herein should be construed otherwise. THE INSIDERS FUND invests in companies at or near prices that management has been willing to invest significant amounts of their own money in. If you would like to hear more about how you can get involved with the Insiders Fund, please schedule some time on my calendar.

Prosperous Trading,

Harvey Sax

The Insiders Fund was the 4th best long-short equity fund in the world in 2019