We’ve added this explanation on put writing from the Options Industry Council. One of our favorite strategies is naked put selling. We only do this on securities we would be willing to own. When we can’t find anything to buy at prices we like ( for example the market has risen to new heights), we may sell puts on stocks we would be willing to buy if they fell back to a level we were comfortable with. If we get put the stock, we are no worse off than had we bought it at that price. If we don’t’ get put the stock, we captured a nice premium and went our merry way. AGAIN NEVER DO THIS STRATEGY AS A WAY TO CREATE JUST INCOME. YOU WILL INEVITABLY GET PUT A STOCK YOU DON’T WANT TO OWN AND THE MONEY YOU MADE ON THE OPTION YOU SOLD CAN BE DWARFED BY THE AMOUNT YOU LOST GETTING OUT OF IT.

Options Strategies: Cash Secured Put

By the Options Industry Council

For Educational Purposes Only

According to the terms of a put contract, a put writer is obligated to purchase an equivalent number of underlying shares at the put’s strike price if assigned an exercise notice on the written contract. Many investors write puts because they are willing to be assigned and acquire shares of the underlying stock in exchange for the premium received from the put’s sale. For this discussion, a put writer’s position will be considered as “cash-secured” if he has on deposit with his brokerage firm a cash amount (or equivalent) sufficient to cover such a purchase

Market Opinion?

Neutral to Slightly Bullish

When to Use?

There are two key motivations for employing this strategy: either as an attempt to purchase underlying shares below current market price, or to collect and keep premium from the sale of puts which expire out-of-the-money and with no value. An investor should write a cash secured put only when he would be comfortable owning underlying shares, because assignment is always possible at any time before the put expires. In addition, he should be satisfied that the net cost for the shares will be at a satisfactory entry point if he is assigned an exercise. The number of put contracts written should correspond to the number of shares the investor is comfortable and financially capable of purchasing. While assignment may not be the objective at times, it should not be a financial burden. This strategy can become speculative when more puts are written than the equivalent number of shares desired to own.

Benefit

The put writer collects and keeps the premium from the put’s sale, no matter how much the stock increases or decreases in price. If the writer is assigned, he is then obligated to purchase an equivalent amount of underlying shares at the put’s strike price. The premium received from the put’s sale will partially offset the purchase price for the stock, and can result in a purchase of shares below the current market price. If the underlying stock price declines significantly and the put writer is assigned, the purchase price for the shares can be above current market price. In this case, the put writer will have an unrealized loss due to the high stock purchase price, but will have upside profit potential if retaining the purchased shares.

Maximum Profit: Limited

Premium Received

Maximum Loss: Substantial

Strike Amount – Premium Received

Upside Profit at Expiration: Premium Received from Put Sale

Net Stock Purchase Price if Assigned: Strike Price – Premium Received from Put Sale

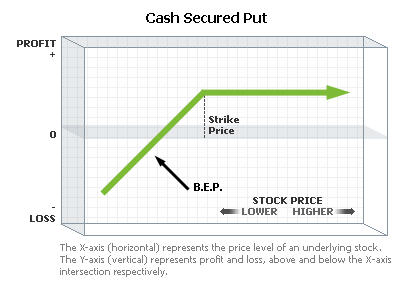

If the underlying stock increases in price and the put expires with no value, the profit is limited to the premium received from the put’s initial sale. On the other hand, an outright purchase of underlying stock would offer the investor unlimited upside profit potential. If the underlying stock declines below the strike price of the put, the investor might be assigned an exercise notice and be obligated to purchase an equivalent number of shares. The net stock purchase price would be the put’s strike price less the premium received from the put’s sale. This price can be less than current market price for the stock when assignment is made.

The loss potential for this strategy is similar to owning an equivalent number of underlying shares. Theoretically, the stock price can decline to zero. If assignment results in the purchase of stock at a net price greater than the current market price, the investor would incur a loss – unrealized as long as ownership of the shares is retained.

Break-Even-Point (BEP)?

BEP: Strike Price – Premium Received from Sale of Put

Volatility

If Volatility Increases: Negative Effect

If Volatility Decreases: Positive Effect

Any effect of volatility on the option’s total premium is on the time value portion.

Time Decay

Passage of Time: Positive Effect

With the passage of time, the time value portion of the option’s premium generally decreases – a positive effect for an investor with a short option position.

Alternatives Before Expiration?

If the investor’s opinion about the underlying stock changes before the put expires, the investor can attempt to buy back the same contract in the marketplace to “close out” his position,thereby realizing a gain or loss. After this is done, no assignment is possible. The investor is relieved from any obligation to purchase underlying stock.

Alternatives at Expiration?

If the short option has any value when it expires, the investor will most likely be assigned an exercise notice and be obligated to purchase an equivalent number of shares. If owning the underlying shares is not desired, the investor can attempt to close out the written put by buying a contract with the same terms in the marketplace. Such a purchase would have to occur before the end of market hours on the option’s last trading day, and could result in a realized loss. On the other hand, the investor is obliged to take delivery of the underlying shares at a possible unrealized loss, in the event of assignment.